tl;dr - summary of interesting articles

The most likely outcome for a startup is failure.

Most seasoned investors and founders operate under the above assumption. There are several risks that skew the outcome towards a failure. Understanding these and mitigating these risks can tilt the scale.

Failure rate for startups. Varies wildly across industries. For example failure in consumer internet is way higher than say mobile hardware

Despite these failures, why do entrepreneurs continue to start companies? naivete, hubris.. or can running a doomed company can actually help a career, yielding experience and networking opportunities with venture capitalists and other entrepreneurs.

The most likely outcome for a startup is failure.

Most seasoned investors and founders operate under the above assumption. There are several risks that skew the outcome towards a failure. Understanding these and mitigating these risks can tilt the scale.

Failure rate for startups. Varies wildly across industries. For example failure in consumer internet is way higher than say mobile hardware

- 30-40% - If failure means liquidating all assets, with investors losing most or all the money they put into the company

- 70-80% - If failure refers to failing to see the projected return on investment

- 90 -95% - If failure is defined as declaring a projection and then falling short of meeting it

--------------------------------------------------------------------------------------------------------------------------

Why Startups fail. Not in any particular order. (Carmen Nobel)

- Lack of foresight or strategy

- Start-ups often fail because founders and investors neglect to look before they leap, surging forward with plans without taking the time to realize that the base assumption of the business plan is wrong. They believe they can predict the future, rather than try to create a future with their customers. Entrepreneurs tend to be single-minded with their strategies—wanting the venture to be all about the technology or all about the sales, without taking time to form a balanced plan.

- Lack of flexibility in the business plan

- And all too often, they do not give themselves wiggle room to pivot midstream if the initial idea doesn't jibe with customer demand.

- Bad timing

- timing can determine whether a company gets funding and whether it achieves the start-up's elusive measure of success: an exit that involves going public or getting bought.

- Lack of funding.

- A company could have a great idea and a great team, but still fail to achieve traction due to lack of funding and, consequently, lack of time to let a good model mature.

Despite these failures, why do entrepreneurs continue to start companies? naivete, hubris.. or can running a doomed company can actually help a career, yielding experience and networking opportunities with venture capitalists and other entrepreneurs.

--------------------------------------------------------------------------------------------------------------------------

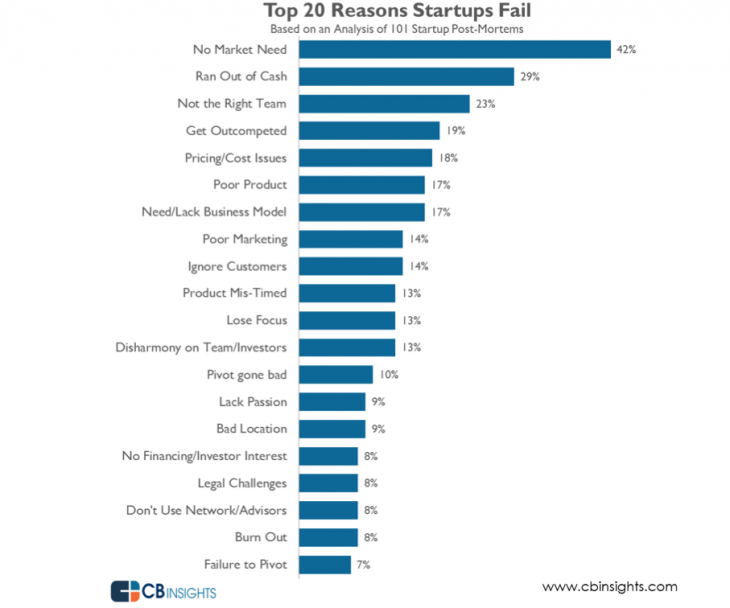

CB Insights 'top 20' list of most common reasons why technology startups fail..

--------------------------------------------------------------------------------------------------------------------------

9 reasons why most startups fail (Entrepreneur)

- Their entrepreneurs live in a vacuum

- Their idea doesn’t uniquely solve a big problem

- They run out of cash

- They invent concepts, not complete products.

- There are big gaps in the strategy.

- The team does not have what it takes.

- Competitors with existing solutions don’t give up so easily

- The market moves on them, or moves in an unexpected way

- They listen to bad advice from the wrong people.

--------------------------------------------------------------------------------------------------------------------------

Top 20 Reasons Startups fail (Businessfinder)

- No revenue from customers

- No input from customers on R&D performed or on the product or service being developed

- Misreading of markets (e.g. overestimate size, delay market entry)

- Product not needed or not simple enough for the application

- Poor sales and marketing decisions (e.g. distribution channels vs. direct sales, delay going global or going global too quickly)

- Timing wrong; the product or service was too early or too late.

- Unaware of competitors and changing market conditions

--------------------------------------------------------------------------------------------------------------------------

Forbes - The Unlucky 13 Reasons Startups Fail

- Market positioning

- No Competitive Research–Wrong Market Positioning

- No Go-To-Market-Strategy

- No focus

- No Flexibility – Know When to Cut Losses

- No Passion or Persistence

- Wrong or Incomplete Leadership

- Unincentivized or Unmotivated Team

- No Mentors or Advisors

- No Revenue Model, Ever

- Less Capital Than Needed – No VC Experience

- No Long Term Roadmap to ROI

- Bad Luck or Timing

--------------------------------------------------------------------------------------------------------------------------

Top 20 Reason Startups Fail ( Chubbybrain.Com )

--------------------------------------------------------------------------------------------------------------------------

http://franchising.clubztutoring.com/reasons-start-ups-fail/

--------------------------------------------------------------------------------------------------------------------------

References

- Why Companies Fail--and How Their Founders Can Bounce Back Author: Carmen Nobel

- http://thenextweb.com/insider/2014/09/25/top-20-reasons-startups-fail-report/

- http://www.entrepreneur.com/article/231129

- http://www.businessinsider.com/the-top-20-reasons-startups-fail-2011-5

- http://www.forbes.com/sites/georgedeeb/2013/09/18/the-unlucky-13-reasons-startups-fail/